Summary

All mutual funds in India have different ‘plans’ – they have a growth plan and a variety of dividend plans. Unlike dividends from stocks, mutual fund dividends are paid out from the fund corpus itself – any dividend then decreases the Net Asset Value of the dividend plan. While mutual fund dividends are tax-free in the hands of the investors, they are subject to Dividend Distribution Tax (DDT). In almost all cases, the combination of DDT and the benevolent taxation on capital gains makes mutual fund dividends a bad choice. So in almost all cases, an investor should use only the growth plan and use redemption’s as required. This article is applicable to India. The suggestion would be unsuitable for other countries – particularly countries like the USA which have legal requirements for dividends from mutual funds.

What are Dividend Plans

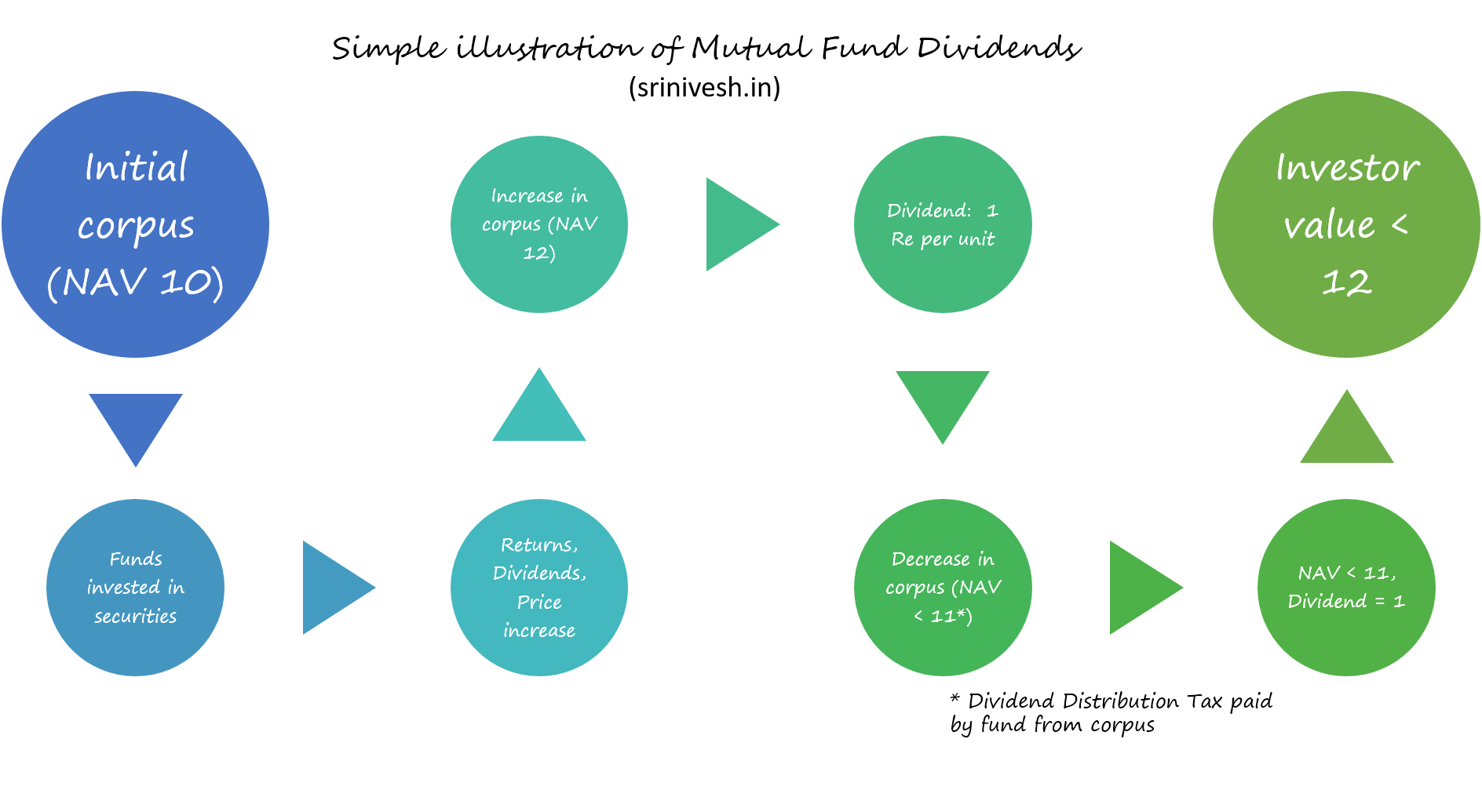

A mutual fund invests the pool of money in a basket of securities. This becomes the corpus of the fund. Interest payments, dividend payments, etc. from the securities are added to the corpus of the fund and this increases the Net Asset Value (NAV) of the units. All the plans of the mutual funds – Growth plan, Dividend plan, Dividend Reinvestment plan – have the same underlying corpus. For Dividend plans, a part of the increase in corpus is paid out in the form of ‘dividends’. This payout results in a corresponding decrease in the NAV of the dividend plan. Here is a simplistic view.

A real-life example of a popular dividend paying fund – HDFC Hybrid Equity – is below. The chart is courtesy mutalfundsindia.com

The chart plots the NAV of the plans for the last five years, with a base of 100. The red line is for the growth plans and the blue line is for the dividend plan. It is evident that the NAV of the growth plan is consistently higher than that of the dividend plan.

Difference between Growth plan and Dividend plan

Let us think of an ideal world where the following assumptions hold:

- Tax treatment of different classes of income is the same

- There are no costs and/or taxes on dividends

- There are no exit loads

In this world, there would be no effective difference between the two plans. In the above picture, the investor could buy one unit each in the dividend plan and growth plan and sell both units after the dividend is received. The net gain of the investor would be Rs 2 each in both plans. For the growth plan, the gain is all in capital gains = 12 – 10, while in the dividend plan, the gain is capital gain = 11 -10, plus Rs 1 of dividend. Alternatively the investor can re-invest the dividend of Rs 1 in the dividend plan again and continue holding them; she would then have Rs 12 worth of investments in both the plans. She would have one unit worth Rs 12 each in the growth plan and approximately 1.091 unit worth Rs 11 each in the dividend plan. (This is what the dividend reinvestment plan does.)

However we don’t live in an ideal world. The next section describes the tax treatment as of 2018.

Tax treatment of dividends and capital gains

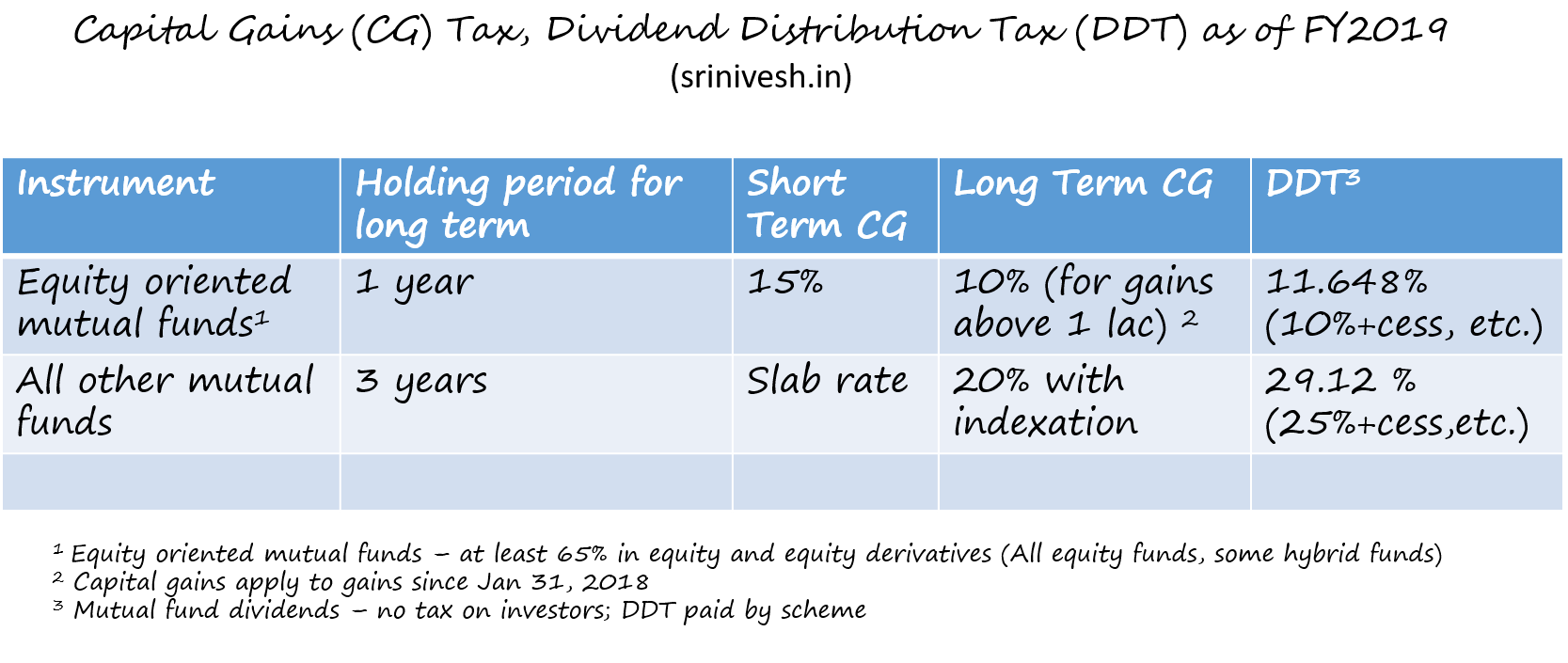

The current tax rules differentiate between equity mutual funds and all other funds for the following factors:

- Definition of long-term

- Tax on capital gains

- Tax on dividend distribution

This table provides an overview of the various parameters.

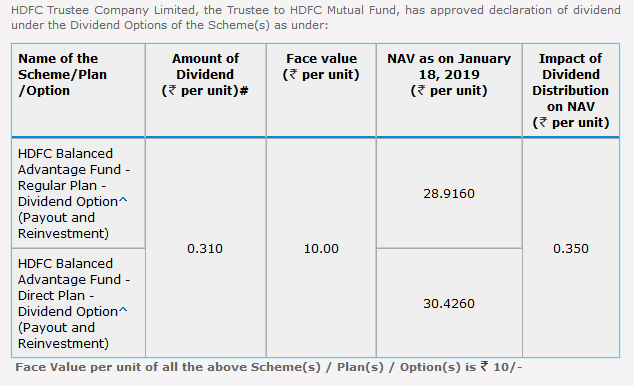

While the dividends are tax-free in the hands of investors, they are levied a Dividend Distribution Tax (DDT). As the dividends come from the corpus of the dividend plan, DDT is also paid out from the corpus. So the reduction in NAV for dividend plans is equal to the sum of dividend plus DDT. The next screenshot gives a real-life example. The dividend to the investor is 31 paise per unit; and the impact on NAV is 35 paise per unit!

The information is courtesy HDFC AMC.

Scenarios where dividend plan could be better

For ease of illustration let us compare two alternate scenarios for an investor who seeks ‘regular’ income from mutual funds.

- The investor invests in growth plans and simply makes redemptions when needed

- The investor invests in dividend plans and uses the dividends for their need

Let us further assume that the dividends are indeed regular and are sufficient for the need. If the funds have crossed the threshold for capital gains, then the following apply.

- For equity funds, for long term, capital gains tax is lower than the DDT and also has an exemption of 1 lac. A dividend of even 1 rupee is subject to DDT.

- For non-equity funds, this difference is wider – capital gains are taxed at 20% with indexation while DDT is much higher

So it is clear that dividend plans are tax-inefficient for long term, even assuming that they are regular in nature.

Most equity funds have an exit load, usually 1%, for redemption made before 1 year. For short term redemptions, the following are the situations where dividend plans could be better.

- For equity funds, STCG is 15%. This plus the exit load of 1% is definitely higher than the DDT

- Of course it really does not make sense to invest in equity for short-term

- For people in the highest tax bracket (30% plus cess, etc.) STCG on debt funds is definitely higher than DDT

- For people in lower tax brackets, for debt funds, STCG rates are definitely lower than DDT

Conclusion

We have seen that there are only a few situations where dividend plans could be better. And these too are with the assumption that the dividends are regular and sufficient. In all the other situations, which would cover most of the real-life situations, growth plans provide the flexibility and more importantly have better overall returns. So instead of chasing dividends, just invest in growth plans of mutual funds.

Came here from the comments on my post in asan group, please insert the exhibit you had shown in the Asan group, under the Tax treatment of dividends and capital gains it gives more clear picture which is based on the example.

Thanks a lot for the suggestion. I have updated the post to include the suggestion.