In the recent days, LIC is running a promotion for its whole life policy – Jeevan Umang. Like any promotion, this campaign highlights the various plus points of the policy, In this article, we compare this investment linked product with a separate investment product and show that it helps to not mix insurance and investment.

Highlights of Jeevan Umang

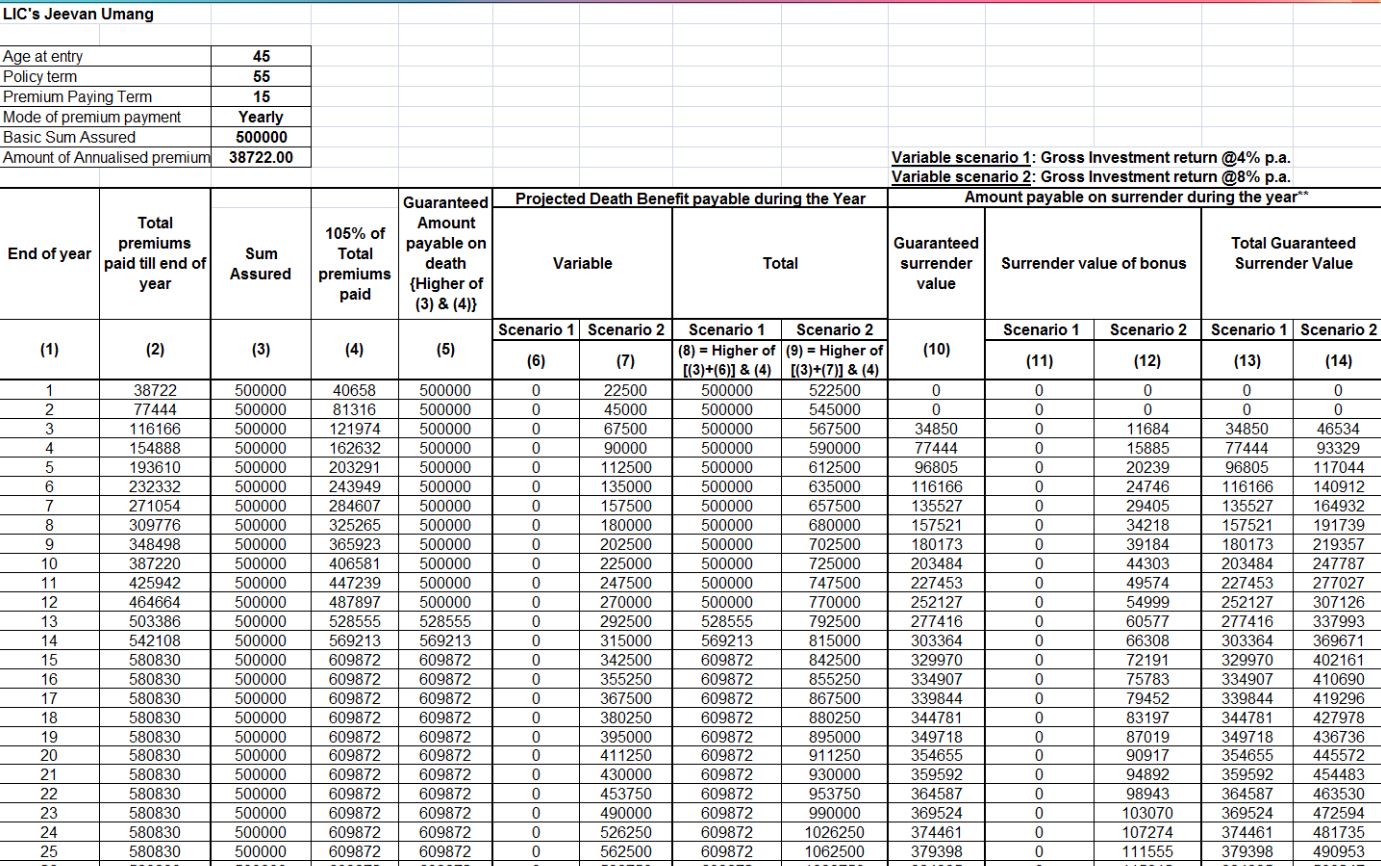

This product is described as a “A non-linked, with-profit, whole life assurance plan”. The very first line in the description of the policy highlights the fact that the plan offers a combination of ‘protection’ and ‘income’. Most whole life plans have a range of policy periods.

Policy Term (PT) – This is the entire age of the policy. Whole life policies generally run till you are 100 years old. For Jeevan Umang, Policy Term = 100 – Your age at entry. For a 45 year old, the policy term is 55 years.

Premium Payment Term (PPT) – It is obvious that one won’t pay premium throughout the period. Usually premiums are paid for 15-30 years. For Jeevan Umang, PPT is fixed for one of these values: 15, 20, 25, 30

Protection Benefits

A life insurance should provide a corpus to the family if the policyholder were to die during the term of the policy. Jeevan Umang adds some bells and whistles on this. The death benefit could be more than the Basic Sum Assured. This can happen due to the addition of annual bonus and additional bonus. Also, the plan guarantees that the death benefit would not be less than 105% of the total premiums paid till date. So after the PPT ends, the death benefit could be more than the Basic Sum Assured even in the absence of any bonus. We would see an example of this in the illustration.

Guaranteed Surrender Value

Once premium has been paid for 3 years, the plan guarantees a surrender value. This is touted as a major benefit of the policy. Frankly, insurance is a long term contract and one should not enter it with the idea of withdrawing after say 5 years. We will ignore this supposed benefit in our analysis.

Survival Benefit

This is clearly a good feature of this plan. After the premium payment term ends, the plan pays a survival benefit every year. This is equal to 20% of the Basic Sum Assured. e.g if the BSA is 5 lac and the PPT is 15 years, the plan pays a sum of Rs 40,000 every year from the 15th year. This continues till the policy ends – on maturity of 100 years or on the death of the policyholder. If one sets up the PPT to end at retirement, this survival benefit could be a part of a pension. This benefit is promoted as such by the agents.

Review of Jeevan Umang plan

A lot of the reviews of this plan, like other LIC plans, are featured by insurance websites. They obviously would claim that this is a great plan. More balanced reviews can be found in financial blogs. This article is one example: LIC Jeevan Umang – New Whole Life Plan | Features, Illustration & ReviewInterestingly, with a set of assumptions, the article calculates the Internal Rate of Return (IRR) to be 5.64%. This is indeed a poor rate of return – even for a tax efficient instrument. However, insurance selles have a habit of highlighting the future cash flows to give an impression that the endowment plan has high returns.In this article, we would use the illustration provided by LIC itself and compare these two approaches:

Approach A – Jeevan Umang plan for Sum Assured of 5 lac and PPT of 15 years

Approach B – A combination of a pure term plan for 15 years, and investment in a pure play financial product (Equity Linked Savings Scheme or Public Provident Fund)

Jeevan Umang – Illustration

The plan at LIC illustration provides a good amount of insight into the workings of the plan. A snapshot is provided below. Please note the two scenarios of return assumptions. The assumptions are for the entire life of the policy. For a large part of the policy term, the projected death benefit is above 6 lac even in the 4% return scenario. The benefit is of course higher in the 8% return scenario.The survival benefit is paid from the 15th year. This amounts to Rs 40,000 per year and is paid every year when the policy is in force. For brevity, this table is not included below.Jeevan Umang – Illustration from LIC

Alternative Approach – Illustration

For this approach, we use these assumptions:

Anmol Jeevan II term insurance for 6 lac for 15 years – this is similar to the guaranteed death benefit for the first approach

The annual premium for this plan for a 45 year old male is Rs 5,381

The rest of the amount of approximately Rs 33,000 is invested in a financial product in a tax efficient way. The two most suitable choices are ELSS and PPF.

The detailed tables illustrate the death and survival benefits from this approach. For the first 15 years, the term policy provides death benefits. In addition, the accumulated corpus provides additional death benefit.

4% Return Scenario

The table below illustrates the death benefit and survival benefit with the assumption that the financial instrument returns 4% post-tax.

4% scenario

End Of Year

Contribution

Sum Assured (A)

Survival Withdrawal

Projected corpus (B)

Projected death benefit (A+B)

1

33,341

6,00,000

0

33,959

6,33,959

2

33,341

6,00,000

0

69,302

6,69,302

3

33,341

6,00,000

0

1,06,084

7,06,084

4

33,341

6,00,000

0

1,44,365

7,44,365

5

33,341

6,00,000

0

1,84,206

7,84,206

6

33,341

6,00,000

0

2,25,670

8,25,670

7

33,341

6,00,000

0

2,68,823

8,68,823

8

33,341

6,00,000

0

3,13,735

9,13,735

9

33,341

6,00,000

0

3,60,476

9,60,476

10

33,341

6,00,000

0

4,09,121

10,09,121

11

33,341

6,00,000

0

4,59,749

10,59,749

12

33,341

6,00,000

0

5,12,439

11,12,439

13

33,341

6,00,000

0

5,67,275

11,67,275

14

33,341

6,00,000

0

6,24,346

12,24,346

15

33,341

6,00,000

40,000

6,43,742

12,43,742

16

0

0

40,000

6,29,969

6,29,969

17

0

0

40,000

6,15,635

6,15,635

18

0

0

40,000

6,00,717

6,00,717

19

0

0

40,000

5,85,191

5,85,191

20

0

0

40,000

5,69,032

5,69,032

21

0

0

40,000

5,52,216

5,52,216

22

0

0

40,000

5,34,714

5,34,714

23

0

0

40,000

5,16,499

5,16,499

24

0

0

40,000

4,97,542

4,97,542

25

0

0

40,000

4,77,813

4,77,813

26

0

0

40,000

4,57,279

4,57,279

27

0

0

40,000

4,35,910

4,35,910

28

0

0

40,000

4,13,669

4,13,669

29

0

0

40,000

3,90,523

3,90,523

30

0

0

40,000

3,66,433

3,66,433

31

0

0

40,000

3,41,362

3,41,362

32

0

0

40,000

3,15,270

3,15,270

33

0

0

40,000

2,88,115

2,88,115

34

0

0

40,000

2,59,853

2,59,853

35

0

0

40,000

2,30,440

2,30,440

36

0

0

40,000

1,99,828

1,99,828

37

0

0

40,000

1,67,969

1,67,969

38

0

0

40,000

1,34,813

1,34,813

39

0

0

40,000

1,00,305

1,00,305

40

0

0

40,000

64,392

64,392

41

0

0

40,000

27,015

27,015

42

0

0

40,000

-11,884

-11,884

43

0

0

40,000

-52,368

-52,368

44

0

0

40,000

-94,502

-94,502

45

0

0

40,000

-1,38,352

-1,38,352

As can be seen, the death benefit is higher than Jeevan Umange for the initial years. However, the withdrawal of the survival benefit reduces the corpus after about 20 years and the corpus dries up after about 40 years. Clearly, if you are a very conservative investor and can generate 4 or 5% returns, you are better off buying the Jeevan Umang policy.

8% Return scenario

Equity Linked Savings Scheme (ELSS) are very comparable to life insurance in terms of tax treatment. The contributions and accumulations are exempt from tax. There is a 10% tax on long term capital gains. For this analysis, we assume a post-tax return of 8%. This is a conservative assumption – almost all ELSS funds can generate much higher returns in the long term.

The table below illustrates the death benefit and survival benefit with the assumption that the ELSS fund returns 8% post-tax. It is clear that this approach is way, way better than Jeevan Umang. For every policy year, the projected death benefit is much higher than the projections for Jeevan Umang.

8% scenario

End Of Year

Contribution

Sum Assured (A)

Survival Withdrawal

Projected corpus (B)

Projected death benefit (A+B)

1

33,341

6,00,000

0

34,591

6,34,591

2

33,341

6,00,000

0

72,053

6,72,053

3

33,341

6,00,000

0

1,12,625

7,12,625

4

33,341

6,00,000

0

1,56,564

7,56,564

5

33,341

6,00,000

0

2,04,149

8,04,149

6

33,341

6,00,000

0

2,55,685

8,55,685

7

33,341

6,00,000

0

3,11,497

9,11,497

8

33,341

6,00,000

0

3,71,943

9,71,943

9

33,341

6,00,000

0

4,37,405

10,37,405

10

33,341

6,00,000

0

5,08,300

11,08,300

11

33,341

6,00,000

0

5,85,080

11,85,080

12

33,341

6,00,000

0

6,68,233

12,68,233

13

33,341

6,00,000

0

7,58,287

13,58,287

14

33,341

6,00,000

0

8,55,815

14,55,815

15

33,341

6,00,000

40,000

9,21,438

15,21,438

16

0

0

40,000

9,57,917

9,57,917

17

0

0

40,000

9,97,424

9,97,424

18

0

0

40,000

10,40,210

10,40,210

19

0

0

40,000

10,86,547

10,86,547

20

0

0

40,000

11,36,729

11,36,729

21

0

0

40,000

11,91,077

11,91,077

22

0

0

40,000

12,49,936

12,49,936

23

0

0

40,000

13,13,680

13,13,680

24

0

0

40,000

13,82,715

13,82,715

25

0

0

40,000

14,57,480

14,57,480

26

0

0

40,000

15,38,450

15,38,450

27

0

0

40,000

16,26,140

16,26,140

28

0

0

40,000

17,21,109

17,21,109

29

0

0

40,000

18,23,960

18,23,960

30

0

0

40,000

19,35,348

19,35,348

31

0

0

40,000

20,55,981

20,55,981

32

0

0

40,000

21,86,627

21,86,627

33

0

0

40,000

23,28,116

23,28,116

34

0

0

40,000

24,81,348

24,81,348

35

0

0

40,000

26,47,299

26,47,299

….

0

40,000

28,27,023

28,27,023

45

0

0

40,000

52,88,269

52,88,269

Best of everything Scenario

Arguments could be made that ELSS are market products and are not suitable for all investors. Let us consider Public Provident Fund (PPF). Like life insurance, this fully exempt from tax. The minimum term of PPF is 15 years and it can be extended for a block of 5 years. The interest rates are aligned to the Gilt yields. Though there has been a downward trend, the rates are still more than 7%. To be on the conservative side, we have assumed a rate of 7% through the term. This instrument is suitable for conservative investors too. Still, this approach provides much better returns than the 8% return scenario in Jeevan Umang.

7% scenario

End Of Year

Contribution

Sum Assured (A)

Survival Withdrawal

Projected corpus (B)

Projected death benefit (A+B)

1

33,341

6,00,000

0

34,432

6,34,432

2

33,341

6,00,000

0

71,353

6,71,353

3

33,341

6,00,000

0

1,10,942

7,10,942

4

33,341

6,00,000

0

1,53,394

7,53,394

5

33,341

6,00,000

0

1,98,915

7,98,915

6

33,341

6,00,000

0

2,47,726

8,47,726

7

33,341

6,00,000

0

3,00,066

9,00,066

8

33,341

6,00,000

0

3,56,190

9,56,190

9

33,341

6,00,000

0

4,16,370

10,16,370

10

33,341

6,00,000

0

4,80,902

10,80,902

11

33,341

6,00,000

0

5,50,098

11,50,098

12

33,341

6,00,000

0

6,24,296

12,24,296

13

33,341

6,00,000

0

7,03,858

13,03,858

14

33,341

6,00,000

0

7,89,172

13,89,172

15

33,341

6,00,000

40,000

8,40,653

14,40,653

16

0

0

40,000

8,61,424

8,61,424

17

0

0

40,000

8,83,697

8,83,697

18

0

0

40,000

9,07,579

9,07,579

19

0

0

40,000

9,33,188

9,33,188

20

0

0

40,000

9,60,648

9,60,648

21

0

0

40,000

9,90,094

9,90,094

22

0

0

40,000

10,21,668

10,21,668

23

0

0

40,000

10,55,524

10,55,524

24

0

0

40,000

10,91,828

10,91,828

25

0

0

40,000

11,30,756

11,30,756

26

0

0

40,000

11,72,499

11,72,499

27

0

0

40,000

12,17,259

12,17,259

28

0

0

40,000

12,65,255

12,65,255

29

0

0

40,000

13,16,720

13,16,720

30

0

0

40,000

13,71,906

13,71,906

….

Note: Partial withdrawals are more restricted in PPF. For ease of analysis, we ignore this small constraint.

Conclusion

Jeevan Umang whole life plan has some good features. However, we have shown that an approach that does not mix insurance and investment provides much better returns, and flexibility, than an endowment insurance product. This is the case even for conservative investors who would prefer government backed instruments.

{kind=link}