Endowment plans are always popular with insurance companies and agents. Due to aggressive positioning, they also become the default choice for many individuals looking for life insurance. In this article, we compare this investment linked product with a separate investment product and show that it helps to not mix insurance and investment.

Features of Endowment Plans

One formal definition of endowment plan is this: a type of insurance in which you pay a regular amount of money over a particular period of time, or until you die, after which the insurance company pays an amount of money. Endowment plans have been always popular with the insurance companies – by pitching the savings aspect, the sales people can avoid talking about grave matters like death.

The savings aspect of the plan comes from the fact that these plans are eligible to share in the profits earned by the insurance company. The insurer invests the premium amount in a variety of avenues, earning returns. Based on the returns earned by it in the year, the insurance provider declares ‘bonus’ on the endowment plans. Many plans could also pay out a final, additional bonus.The bonus declared every year could be even higher than the premium amount. This is used as a selling point. However, this bonus is not compounded and is simply added to the corpus when it is paid out.Compared to a simple term insurance, these policies have a higher premium; this is seen as a benefit by people focusing on tax deductions under Section 80(c). The biggest advantages of endowment plans could be these:

Disciplined saving

Payment at the time of maturity

Reasonably known rate of return

Possibility of using policy as loan collateral

The disadvantages should actually outweigh the benefits, though many investors fail to see them.

Low insurance cover for premium paid

Low surrender values are not typically disclosed

Returns are lower compared to market instruments

We would look at the last point in detail and show that returns on a popular endowment plans are much lower than a reasonably assured return product like Public Provident Fund. One article that discusses endowment plans’ features is here. Yes, these plans exist in many other countries too.

Review of popular Jeevan Labh plan

Jeevan Labh from LIC is described as a “Limited premium paying, non-linked, with-profits endowment plan which offers a combination of protection and savings.” A lot of insurance focused sites, blogs, etc.term this as one of the best endowment plans with high returns. A lot of the reviews of this plan, like other LIC plans, are featured by insurance websites. They obviously would claim that this is a great plan. More balanced reviews can be found in financial blogs. This article argues against the plan and asks if there is “LABH in Jeevan Labh”With liberal assumptions on the bonus, the article calculates the annualized return to be between 6 and 7%. This is indeed a poor rate of return – even for a tax efficient instrument. However, insurance sellers have a habit of highlighting the future cash flows to give an impression that the endowment plan has high returns.In this article, we would use the illustration provided by LIC itself and compare these two approaches:

Approach A – Jeevan Labh plan for Sum Assured of 2 lac, term of 25 years and PPT of 16 years

Approach B – A combination of a pure term plan for 25 years, and investment in a pure play financial product – Public Provident Fund

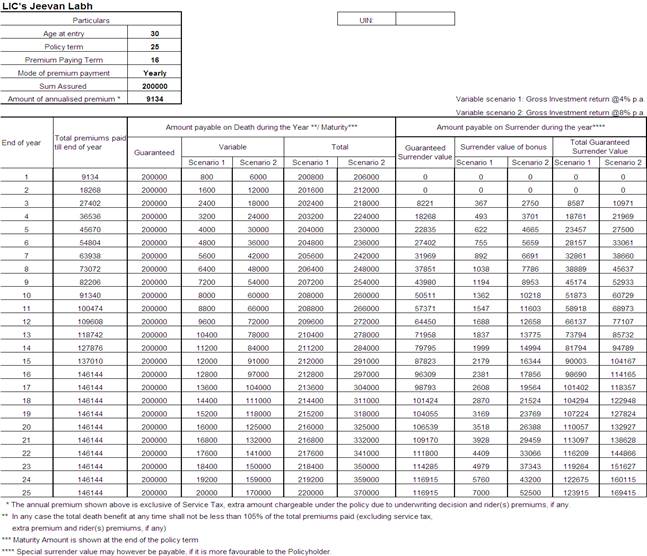

Jeevan Labh- Illustration

The details at LIC illustration provides a good amount of insight into the workings of the plan. A snapshot is provided below. Please note the two scenarios of return assumptions. The assumptions are for the entire life of the policy. For a large part of the policy term, the projected death benefit is above 2 lac even in the 4% return scenario. The benefit is of course higher in the 8% return scenario. Jeevan Labh – Illustration by LICThe illustration image is a bit difficult to read. For comparison, please look at the various values (over the years) in the Variable column for Scenario 2. Assuming an 8% return, this amount is s 30,000 at the end of the 5th year, 60,000 at 10th year, and so on, going up to 1,70,000 at the end of the 25th year. The insurance agents would compare this with the total premium paid – about Rs 1,40,000 – and show how you are getting a lot of returns. We would show that this is not really the case.

Alternative Approach – Illustration

For this approach, we use these assumptions:

Anmol Jeevan II term insurance for 3 lac for 25 years – this is similar to the guaranteed death benefit for the first approach

The annual premium for this plan for a 30 year old male is taken as Rs 2,200 (The lowest sum assured in Anmol Jeevan II is 6 lacs and the premium is Rs 2,506. We have taken a slightly lower value for half the sum assured)

The rest of the amount of approximately Rs 6,900 is invested in a financial product in a tax efficient way. The two most suitable choices are ELSS and PPF. For this comparison, we choose PPF.

Returns in Alternative Scenario

Arguments could be made that ELSS are market products and are not suitable for all investors. Let us consider Public Provident Fund (PPF). Like life insurance, this fully exempt from tax. The minimum term of PPF is 15 years and it can be extended for a block of 5 years. The interest rates are aligned to the Gilt yields. Though there has been a downward trend, the rates are still more than 7%. To be on the conservative side, we have assumed a rate of 7% through the term. This instrument is suitable for conservative investors too. Still, this approach provides much better returns than the 8% return scenario in Jeevan Labh.The detailed table illustrates the death and survival benefits from this approach. For the term of 25 years, the term policy provides death benefits. In addition, the accumulated corpus provides additional death benefit. Right from the first year, this approach provides a better benefit than the endowment plan. After 25 years, the accumulated corpus is available as ‘maturity benefit’. The projected corpus of > 3.8 lacs is more than the maturity benefit from the endowment plan. And to top this, the corpus can be continued further if needed for blocks of five years, earning additional returns.

7% scenario

End Of Year

Contribution

Sum Assured (A)

Projected corpus (B)

Projected death benefit (A+B)

1

6,934

3,00,000

7,161

3,07,161

2

6,934

3,00,000

14,839

3,14,839

3

6,934

3,00,000

23,073

3,23,073

4

6,934

3,00,000

31,902

3,31,902

5

6,934

3,00,000

41,369

3,41,369

6

6,934

3,00,000

51,520

3,51,520

7

6,934

3,00,000

62,405

3,62,405

8

6,934

3,00,000

74,078

3,74,078

9

6,934

3,00,000

86,593

3,86,593

10

6,934

3,00,000

1,00,014

4,00,014

11

6,934

3,00,000

1,14,405

4,14,405

12

6,934

3,00,000

1,29,836

4,29,836

13

6,934

3,00,000

1,46,383

4,46,383

14

6,934

3,00,000

1,64,126

4,64,126

15

6,934

3,00,000

1,83,151

4,83,151

16

6,934

3,00,000

2,03,552

5,03,552

17

0

3,00,000

2,18,267

5,18,267

18

0

3,00,000

2,34,046

5,34,046

19

0

3,00,000

2,50,965

5,50,965

20

0

3,00,000

2,69,107

5,69,107

21

0

3,00,000

2,88,561

5,88,561

22

0

3,00,000

3,09,421

6,09,421

23

0

3,00,000

3,31,789

6,31,789

24

0

3,00,000

3,55,774

6,55,774

25

0

3,00,000

3,81,493

6,81,493

Conclusion

Jeevan Labh endowment plan has some good features. However, we have shown that an approach that does not mix insurance and investment provides much better returns, and flexibility, than an endowment insurance product. This is the case even for conservative investors who would prefer government backed instruments.

{kind=link}

1 thought on “Avoid Endowment Plans – PPF gives better returns”