‘Free’ advice costs you a lot

There are many articles that try to establish why regular funds are more suitable for investors. Almost all of them use the following scenarios/models:

- Advisor/platform providing free advice and logistics for investments in regular funds (free advice model)

- An investor doing everything themselves and investing in direct funds (Do It Yourself or DIY model)

In this article, I illustrate a model where a naive investor consults with a fee-only financial planner and invests in direct mutual funds recommended by the planner. I show that this investor comes out ahead in spite of spending on fees and logistics.

Typical ‘free’ advice model

This model is implemented by many mutual fund distributors, online platforms, etc. In this model, the investor is helped in many ways to come up with her investment needs. She is also helped to decide the required investments among debt, equity, etc. The advice may also cover insurance needs. She is helped in completing the logistics – getting KYC done, setting up ECS or other standing instructions, etc. The mutual funds investments are set up in regular funds. In most cases, she is helped with periodic review of the portfolio. She also has access to personal relationship manager whenever needed.

The argument then is that this model is better, particularly for new investors, mainly based on the following factors:

- Fund selection

- Logistics like KYC, payment mechanisms, etc

- Tracking of investment performance (since the distributor gets a feed)

- And more importantly, emotional support through the investment years

These advantages then supposedly more than compensate for the higher expense ratio incurred in regular funds. An example is here. In a typical DIY model, the above take time, knowledge and a lot of self-discipline. However, not every one needs a DIY model. A different model exists and is more suitable.

A suitable ‘paid for’ advice model

Let us assume that the investor is new and just getting started with their financial plan. Instead of trying to do this herself, she can consult with a fee-only financial planner. This person is certified by SEBI as a Registered Investment Advisor and has undertaken to not earn any sort of commission from the recommendations provided by them. A list of fee-only financial planners can be found here.

The planner would spend a good amount of time with the investor and come up with a suitable financial plan that meets her goals. Typically this plan would be better than, or at least as good as, the plan from the free advice model. The plan would also cover insurance needs. The planner charges an one-time, flat fee for this. Many planners have a fixed amount that includes consultations for 1 year. Some of the planners charge a percentage of the corpus as fees. (For this article, we would focus on the flat fee model.) Almost always, there is an option to do yearly review and revision of the plan, for an additional fee.

Once the plan is developed, the investor often has to set start investing on her own. With platforms like MFU, myCAMS, etc. this is not difficult at all. There is a small initial hump to get KYC completed and do the first investment(s).

After the initial steps, the investor can continue to consult with the planner as needed. And yes, seek all the support required in handling tough situations, including market corrections. The investor can also choose to pay for subsequent reviews of the plan. Often the planner and the investor will set up a mechanism to track the portfolio – the Consolidated Account Statement (CAS) is enough for this.

In summary, an investor can pay a fee and get every supposed benefit provided by the distributors.

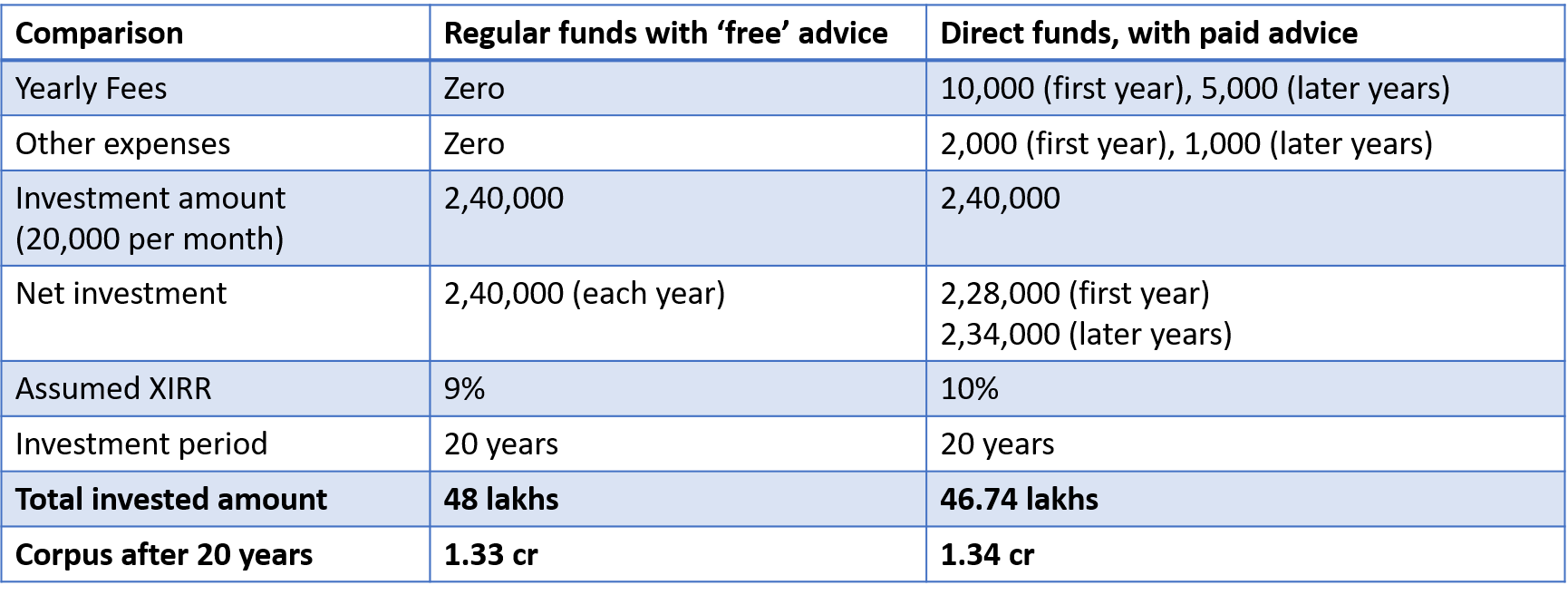

Comparison of costs and returns

To focus on the comparison, I have used a simple situation. We assume that the planning has been completed and the person needs to invest 20,000 per month in equity mutual funds. In the paid model, I deduct the fees from the investment amount; I also deduct costs for setting up logistics. Direct funds have completed more than five years now and many equity funds show a return difference of 1% or more between the regular and direct plans. One comparison is below:

This comparison is loaded against the paid advice model. Still, the paid advice model comes out a bit ahead. Since the fee is flat and the commission is based on the corpus, the flat fee model only gets better and better, as the corpus increases and more investments are made.

Edit: An argument can be made that the review fees may increase beyond Rs 5,000 in latter years. This is indeed possible. This is compensated by the fact that the review fees are actually lower than Rs 5,000 for most fee-only advisors.

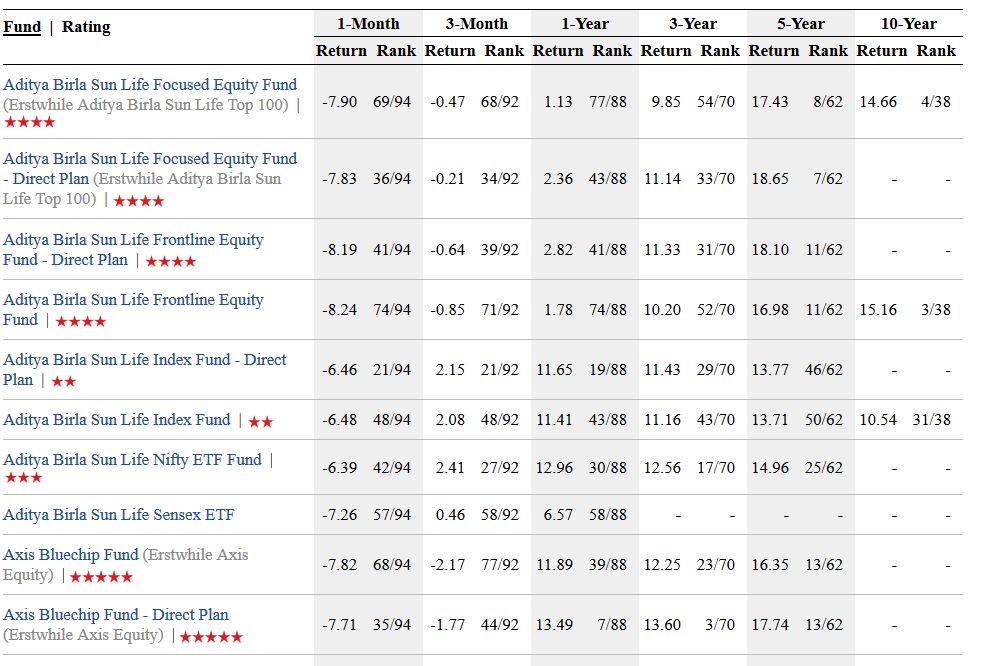

Edit: Direct plans of mutual funds have been available since Jan 1, 2013. The 5+ years of data establishes clearly the difference in returns between direct and regular plans. Below is a partial list of returns for the top 15 large cap funds in India. The list includes both direct and regular plans, usually right next to each other. You can see that the active funds have a difference of 1% more in CAGR.

Conclusion

Comparing the free advice model with a DIY model may show the DIY model to be less suitable for investors, particularly less experienced investors. However the right comparison is between the free advice model and paid advice model. In such a comparison, the free advice model comes out less advantageous.

To put it simply: Pay for good advice, and invest in direct mutual funds. You would come out better.

Additional Reading:

Hi,

Nice post.

Just an observation on your table.

1. Fee only adviser may not continue to charge Rs5000 for next 18-19 years. Ideally that should be indexed to inflation and fee should be increased.

2. “Direct funds have completed more than five years now and many equity funds show a return difference of 1% or more between the regular and direct plans.” would be good if you can put another chart with mutual funds and their returns in direct and regular investment.

Thanks

Prateek

Thank you for the comments.

1. Yes, it is possible for the review fees to increase. I would include an inflation factor in the next version of the table.

2. Thanks for the suggestion. This is reasonably simple to do from the wealth of data available. I would consider a specific blog post on this.