Unit Linked Insurance Plans (ULIPs) have always been aggressively positioned in India. The recent (re)introduction of Long Term Capital Gains (LTCG) Tax on equity has added another dimension to the promotion of ULIPs. In this illustrative post, we look at how Equity mutual funds still provide better post-tax returns due to their flexibility and choice.

What are ULIPs

We assume that the reader is familiar with ULIPs. In short these products combine investment with insurance. Your investment (net of charges) goes into a fund that works just like a mutual fund. The funds are managed by the insurer and you have to choose only from the handful of options. Fund management charges, as well as the insurance charges, are deducted from the value of the fund.

For more information, you can read this link from HDFC Life. (For illustration, this articles uses information on products from the HDFC group.)

Comparison Scenario

Since insurance itself is a must-have for any investor, the appropriate comparison would be this: a) ULIP vs b) Mutual Funds + Term Insurance. We would use this comparison. To help the comparison, all the assumptions will be biased in favour of ULIPs.

Insurance Charges/Mortality rates

In a term insurance plan, the premium amount is paid as per the schedule. In an ULIP, the mortality charges are deducted from the fund value by cancelling units. Mortality charges themselves are well researched and regulated. For simplicity, we will assume that the effect on the investible amount is the same in both cases. i.e. The buyer pays 16,000 for the ULIP (of which Rs 1,000 is used for mortality charges); for the second scenario, the buyer pays Rs 1,000 for the term insurance premium and invests Rs 15,000 in the chosen mutual fund.

Fund Management Charge/Expense Ratio

In mutual funds, the published NAV is net of expenses. The ULIP funds deduct a fund management charge. It is not clear if the indicated returns are inclusive of the charges are net of the charges. Some insurers suggest that the daily unit price is net of charges. An example is the statement from HDFC Life:

“The daily unit price is calculated allowing for the deduction of the fund management charge, which is charged daily.”

For simplicity, we would assume that the returns are net of the charges for ULIPs. This then makes them similar to mutual funds. (Note: Most direct plans in equity have TER comparable to or less than typical fund management charges. For debt, the fund management charges are higher than the TER of debt funds.)

Other charges

There are plans, particularly online, which have low or zero other charges – premium allocation charges, administrative fees, etc. For simplicity, and to err on the side of ULIPs, we would ignore all these charges.

The three comparisons put together make the comparison straightforward – we directly compare the published returns and expected returns.

ULIP choice

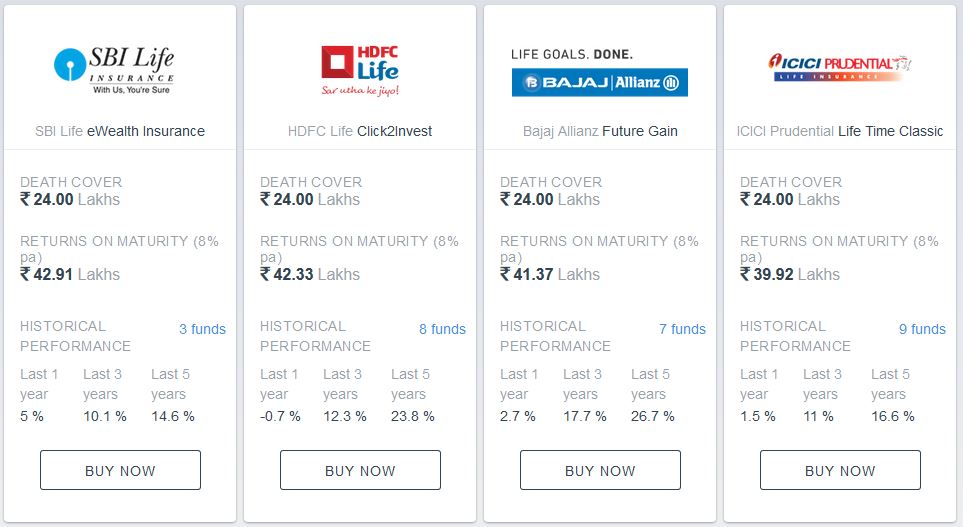

Every life insurance provider in India has a number of ULIP products. A lot of these companies also have associates in the mutual fund business – SBI Life and SBI AMC; HDFC Life and HDFC AMC; ICICI Pru Life and ICICI Pru AMC, etc. The insurance comparison websites provide a view of the various features of the ULIPs. One such comparison is below. (Assumption: Payment of Rs 20,000 every month for 12 years)

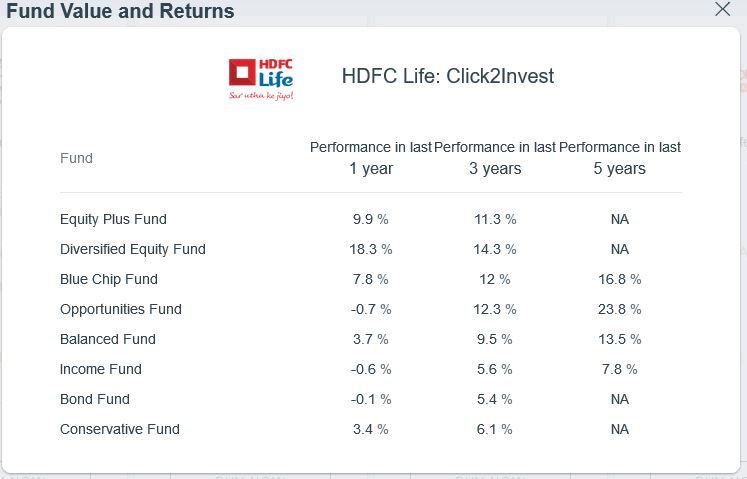

The difference in estimated returns is due to the variety of charges. The historical performance of the funds, as well as the choice of funds, vary across the insurers. Balancing all the factors, we would choose HDFC Life Click2Invest The performance snapshot of the 8 funds is below.

Among the funds, we would choose the Blue Chip Fund. Based on this, we would also select the category of large cap in mutual funds. Large cap funds provide a better balance of risk and returns. If one wants to use the data for Opportunities Fund, the appropriate mutual fund category would be multi-cap funds. To bias for ULIPs, we can check that among the ULIP large cap funds, HDFC Life’s fund indeed has the best 5 year performance.

Mutual Fund choice

Since we have picked a large cap fund from the ULIP space, we would look at the large cap category. A quick selection in VRO gives us the following list. You can easily see that many of the well performing mutual funds easily outperform the ULIP funds, based on published returns.

Open-ended – Equity: Large Cap – Return Five Year – Top 10

| Fund | Rating | Category | Launch | Expense Ratio (%) |

5-Year Return (%) |

5-Year Rank |

Net Assets (Cr) |

|---|---|---|---|---|---|---|---|

| Reliance ETF Junior BeES | Invest Online |  |

Feb-2003 | 0.23 | 20.35 | 1/62 | 542 | |

| JM Core 11 Fund | |

Mar-2008 | – | 20.24 | 2/62 | 36 | |

| Reliance Large Cap Fund | Invest Online |  |

Aug-2007 | 2.30 | 20.09 | 3/62 | 11,601 | |

| ICICI Prudential Nifty Next 50 Index Fund | Invest Now | |

Jun-2010 | 0.85 | 19.83 | 4/62 | 300 | |

| IDBI Nifty Junior Index Fund | |

Sep-2010 | 1.74 | 18.83 | 5/62 | 53 | |

| SBI Bluechip Fund | Invest Online | |

Feb-2006 | 2.35 | 18.10 | 6/62 | 20,702 | |

| HDFC Top 100 Fund | Invest Online |  |

Sep-1996 | 2.02 | 17.49 | 7/62 | 15,874 | |

| Aditya Birla Sun Life Focused Equity Fund | Invest Online | |

Oct-2005 | 2.36 | 17.42 | 8/62 | 4,263 | |

| ICICI Prudential Bluechip Fund | Invest Now | |

May-2008 | 2.08 | 17.17 | 9/62 | 19,836 | |

| Motilal Oswal Focused 25 Fund – Regular Plan | Invest Online | |

May-2013 | 2.38 | 17.10 | 10/62 | 1,171 |

Comparison of Net Returns

With the information that we have collected so far, we look at the returns from the two scenarios. Since mutual funds have more flexibility and better overall returns, we have assumed a difference of 1.5% in the returns compared to ULIPs.

| Comparison | ULIP | Mutual Fund |

| Provider | HDFC Life | HDFC AMC |

| Plan Name | HDFC Life BlueChip Fund | HDFC Top100 Direct |

| Investment amount

(15,000 per month) |

1.8 lac per year | 1.8 lac per year |

| Investment period | 20 years | 20 years |

| Assumed XIRR | 12% | 13.5% |

| Total invested amount | 36 lacs | 36 lacs |

| Corpus after 20 years | 75.15 lac | 85.99 lac |

| Taxes | 0 | 4.99 lac |

| Net corpus after tax | 75.15 | 80.99 |

Wait, what about 80(c) savings

It is true that the entire amount of Rs 16000 has tax deductions in the case of ULIPs. For the second scenario, only the term insurance premium of Rs 1,000 is tax exempt. One can always choose ELSS funds tax deductions. Also, most investors have enough ways to fill up the 80(c) limit without having to buy a high cost product like ULIP. (Please see this article for a partial list.)

For other supposed advantages of ULIPs over mutual funds, you can read this article: Do not buy ULIPs because equity mutual fund LTCG will be taxed!

Conclusion

In this comparison, we loaded the odds in favour of ULIPs. The only advantage provided to mutual funds was the assumption of higher returns. In spite of the unfavourable odds, we see that mutual funds can be expected to give a higher corpus even after accounting for taxes. So continue to say a big NO to ULIPs.

I understand that you loaded the comparison in favor of ULIPS. But would you then say that if the ULIP fund were to give as good returns as the mutual fund, then ULIP is better?